LEVR™

A better way to repay. A smarter way to buy.

LEVR™ replaces the old payment-calculator story with a repayment automation system built to help people pay down term loans while eliminating late payment fees. Consumers build equity and/or recover from negative equity faster and in a way that works better with how families budget. Weekly > Monthly where term loan repayment plans.

Instead of making only 12 monthly payments in a 12-month calendar year, LEVR helps structure repayment so the customer effectively makes the equivalent of 13 or 14 monthly payments in that same year (consumer’s choice). LEVR’s patented innovation: weekly micro-payments that create the equivalent of 13 or 14 months worth of payments in 12 months. 14 payments in 12 months example: Can produce +16.7% additional principal reduction annually and make an 84-month loan behave more like a 68-72 month payoff.

That is the shift.

Not just what can I buy today?

But what is the better way to repay so I keep more money, build equity faster, and get ahead sooner?

Our Patented MY Payment Power SRP/VDP Conversion Technology Represents a Seismic Shift Online Engagement & Conversion

By setting up 13 or 14 monthly payments in a calendar year, users can pay off term loans months sooner, eliminate late fees, and reduce interest paid over time. The service also offers features like rounding up daily debit card purchases to accelerate loan repayment.

What LEVR™ does

LEVR™ helps turn a standard term loan into a smarter repayment path.

That means:

- smaller weekly repayment behavior

- the equivalent of 13 or 14 payments in a 12-month year

- faster principal reduction

- less interest paid over time

- fewer late-payment problems

- stronger equity position

- more financial confidence for the customer

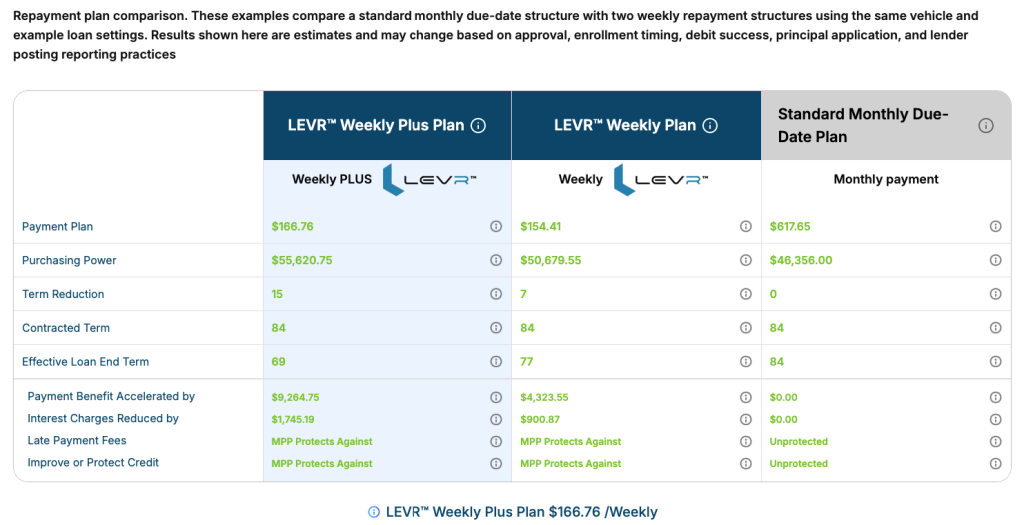

Internal LEVR™ materials define this as an “Effective Loan Term” advantage created by accelerated principal payoff through 13 or 14 payments in a 12-month calendar year .

How it works

The old way

Most term loans are built around:

- 12 payments per year

- standard amortization

- slower principal reduction

- a higher chance of falling behind when monthly timing gets tight

The LEVR™ way

LEVR™ uses smaller, more frequent repayment behavior to help the customer effectively make:

- 13 payments per year, or

- 14 payments per year

That means more money reaches principal sooner.

And when principal falls faster:

- the loan term shrinks

- total interest charges fall

- equity improves sooner

- the customer is less likely to stay underwater

Internal LEVR™ documents are clear that traditional banking systems are generally not set up to attack principal this way, and that most traditional banks and nationwide finance companies are unwilling or unable to replicate the 13-or-14-payments-in-12-months structure .

MY PAYMENT POWER™ OFFERS A SOLUTION!

Why 13 or 14 payments matters

One extra payment changes the pace.

Two extra payments changes the outcome.When a customer makes the equivalent of 13 or 14 monthly payments in one calendar year:

- principal goes down faster

- interest has less time to build

- payoff comes sooner

- equity improves sooner

- late-fee risk can fall

- the customer has a better chance to afford the vehicle or home they want instead of settling for the one they think they can survive

LEVR’s 14-payment version is the equivalent of making 2 extra principal payments per year.

What it does for the customer

Faster payoff

A standard loan can begin to act like a shorter loan when extra principal is pushed down earlier. An 84-month vehicle loan can behave more like a 68-72 month payoff under the 14-payment structure and for a 16+ year term loan a 30-year loan can behave more like an 18-23 year loan.

Lower interest burden

When principal falls sooner, the customer pays less interest over the life of the loan.

Better equity

Paying down the balance faster helps the customer build equity sooner and reduce the chance of staying trapped in negative equity.

Smaller, more manageable rhythm

Weekly micro-payments are easier for many households to manage than one larger monthly hit. Internal LEVR™ materials frame this as a behavioral advantage that reduces delinquency risk because the payment size is smaller and more frequent .

Fewer late-payment problems

More frequent repayment can help customers avoid getting too far behind before anyone notices (while a relative or friend can afford to bridge their shortfall and help get them back on track).

What it does for the dealer

Helps the dealer sell the right vehicle, not just the cheaper vehicle

LEVR™ helps shift the conversation away from “What monthly payment scares me least?” and toward “What repayment path helps me afford the vehicle I really want and keep it in a healthier way?”

Improves customer confidence

A shopper who sees a smarter repayment path is more likely to move forward.

Builds equity faster

Customers who build equity sooner create healthier future trade cycles.

Reduces payment-shock discounting

Internal materials note that payment-shock discounting damages margin and that smarter repayment structures help reduce that pressure .

Creates a stronger trust story

The dealer gets credit for helping stabilize household finances instead of just selling metal.

Supports recurring transaction value

LEVR™ helps move the dealership from a one-time sale mindset toward a longer financial relationship tied to the customer’s repayment path.

What it does for media companies

Unlocks access to non-traditional transactional revenue

LEVR™ gives media companies a way to participate in big-ticket sell/trade and buy/lease transactional revenue streams, not just ad impressions or traffic monetization.

Connects media to the transaction, not just the click

LEVR™ aligns media companies as demand engines, banks as more friendly financing, repayment and loan default prevention engines. As local inventory providers, with AutoPLai as the infrastructure layer, LEVR is a Community-Connected Commerce core solution. With LEVR™, media companies are no longer stuck on the outside of the transaction (selling attention only).

Creates recurring value after the sale

AutoPLai℠ is combining marketplace transactions, media distribution, financial services, and long-term recurring payment revenue . LEVR™ is the repayment layer that helps turn the initial transaction into a longer-duration revenue relationship.

Gives media a stronger community-finance story

LEVR is not just another payment ad. It is a better-repayment story that media companies can bring to market as something useful for households, dealers, and local lenders.

Supports Community-Connected Commerce™

Instead of using media only to drive traffic, LEVR™ helps media companies take part in a local commerce system tied to:

- real transaction activity

- financing outcomes

- recurring payment behavior

- retained local value

What LEVR™ does for financial institutions

Better repayment behavior

LEVR gives lenders a structure built around smaller, more frequent repayment.

Lower risk exposure

Internal LEVR materials describe weekly repayment and accelerated principal reduction as a dynamic risk model with:

- weekly repayment data

- real-time cash flow visibility

- reduced exposure duration

Faster problem detection

Internal documents state that this structure can help detect repayment problems in 1–2 weeks instead of 2–3 months.

A more client-friendly & considerate repossession and foreclosure prevention engine. Lenders get a new approach to late payment or default risk with LEVR’s “get back on track” term loan (late or near-defaulting) cure options.

Stronger lender confidence

LEVR leans into delinquency risk prevention giving lenders and their customers real-time cash flow automation to reduce risk of late fees and loan defaults.

Participation in recurring repayment-linked revenue

LEVR™ helps financial institutions stay connected to a better-structured repayment relationship rather than only the original booking event.

What makes LEVR™ different

Most payment tools answer one question:

“What is my payment?”

LEVR™ answers a more important one:

“What is the better way to repay?”

That is the difference between:

- showing a number

and - changing the upfront choices and outcome

LEVR is not just a Big Ticket Item payment calculator.

It is a patented repayment structure designed to:

- reduce financial friction

- improve payoff timing

- reduce interest burden

- improve equity outcomes

- give dealers, media companies, and financial institutions a shared reason to support the system

Key features

Our patented solution includes LEVR-Optimized:

- Weekly micro-payment structure

- 13-payment annual equivalent option

- 14-payment annual equivalent option

- Faster principal reduction

- Reduced interest burden over time

- Earlier payoff potential

- Better equity-building support

- Lower late-fee risk exposure

- Stronger lender monitoring rhythm

- Dealer, media, and financial-institution alignment around better repayment behavior

- Access to non-traditional big-ticket transactional revenue streams

- Recurring repayment-linked value after the initial sale

Why it matters

Today’s shopper is dealing with:

- inflation

- high rates

- high vehicle costs

- negative equity

- financial uncertainty

LEVR™ gives all sides a smarter answer.

For the customer, it creates a better path to ownership.

For the dealer, it helps support stronger deals and healthier future trades.

For the media company, it unlocks access to non-traditional big-ticket sell/trade and buy/lease transactional revenue streams.

For the financial institution, it creates a lower-risk repayment structure with better ongoing visibility.

LEVR™ helps people repay smarter, not just borrow longer.

When customers make the equivalent of 13 or 14 monthly payments in a 12-month calendar year, they can pay down principal faster, reduce interest burden, improve equity sooner, and move toward ownership with less friction.

That is better for the customer.

Better for the dealer.

Better for the media company.

Better for the financial institution.

And better for our partners helping bring the system to market.